Editor’s note: Seeking Alpha is proud to welcome Very Thirsty For Dividends as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

utah778

Thesis Summary

I present a hybrid investment strategy that can be implemented for improving the total return of portfolios containing high yield dividend stocks. The specific mechanics for managing each stock in the portfolio utilizing this strategy are: (A) When the stock’s yield falls below a user-optimized level (the so-called “cut-off” level), accumulate stock dividends as cash and maintain the cash along with stock shares in the portfolio and (B) if the stock yield increases above that same level, convert all accumulated stock portfolio cash associated with each stock into stock shares and reinvest the dividends as more shares.

I have executed several cases for comparison, but specifically and initially for the stocks Altria (MO), AbbVie (ABBV), Texas Instruments (TXN) and Edison International (EIX). These stocks are more suitable candidates for employing this strategy due to their historically higher yields (well exceeding S&P 500 yields) and regular yearly dividend increases. None of these companies suspended or reduced dividends within the past ten years and they all are chosen from different sectors.

I have demonstrated in this analysis that the hybrid (or “selective yield”) methodology, implemented in the fashion highlighted above for the four portfolio component stocks MO, ABBV, TXN and EIX can produce as much as a 15-20% average improvement in annualized returns for each stock position in the portfolio, over the case where no dividends are reinvested for each of these portfolio component stocks.

Following this stock optimization process for managing the performance of the above stocks individually, I then combine the four stocks into one portfolio and analyze the total return performance of the entire portfolio, both without reinvesting dividends, and then for selectively reinvesting dividends for the selected and specified cut-off yields for each stock.

Strategy Introduction

Investing in higher yielding dividend stocks such as Altria, AbbVie, Texas Instruments, and Edison International can be a powerful vehicle for accumulating dividends and enhancing portfolio value for the income-oriented investor.

The so-called “hybrid strategy” is a methodology that an investor can deploy with varying degrees of success in a portfolio of dividend-paying stocks. This procedure involves selectively reinvesting dividends only when the stock yield is above a prescribed level, otherwise allowing the dividends to be declared in cash, and maintained in a money market account until the stock yield once again rises above a fixed level, at which point the accumulated cash is converted into stock shares, and the dividends are once again reinvested into more stock shares.

Technique (Analytics)

The main (quarterly) calculations employed in this model are: a) the reinvestment of dividends as shares, b) the conversion of cash to shares when the stock yield rises above a user-selected level, c) the separate compounding of cash in the portfolio and incrementing dividends as cash when the yield is below the user specified level, and d) the combined cash plus share value which generate the total value in the portfolio. These are (note ps= “per share”, * = multiplication (X)).

(A) new_shares = old shares + (dividend(ps)*old shares/price).

(B) shares = new_shares (in A above) + cash/price (ps).

(C) cash new = (cash old + dividend (ps)*old shares)*(1+rate_fixed/100).

(D) portfolio_value (US dollars $) = shares*price (ps) + total cash.

I will be glad to provide more in-depth details as to the computer model and the equations it employs in this methodology, but for the present, I do not want to get bogged down into intricate details, but would rather focus on the results and usefulness of the model employed. Again, I have applied this technique to four individual stock candidates – ABBV, MO, TXN and EIX – for optimization of the reinvestment of dividends for each stock separately. These stocks were selected because they are higher-yielding stocks whose dividends are regularly are increased yearly. For now, the initial point of focus for me is to include equal US Dollar ($) amounts for each of the four stocks initially in the composite portfolio.

Model Execution and Results

I have carried out computations for an investment time interval between September 30, 2013, and June 30, 2023, for each of the stocks considered (MO, ABBV, TXN and EIX).

Please note that I have utilized data based upon composite chart data obtained from Fidelity Investments Website. For example, here is a stock chart for MO over the timeframe selected. I employed a similar chart for ABBV, TXN and EIX, although the dates for dividend declaration do not exactly overlap.

Fidelity.com

Note that reinvestment prices are approximate. I used the end-of-the-month prices as approximate reinvestment prices and also the dividends declared during the same month in which dividends were scheduled to be declared.

I also employed as a reference comparison a chart of the S&P 500 Index (SP500), also provided on the Fidelity Investments Website. Note that the price chart for the SP500 does not include dividends reinvested.

Fidelity.com

I basically ran three fundamental cases for all four stocks, which I have included in chart form on Excel spreadsheets, and then provided a tabular summary of the results in a separate Excel sheet. The initial investment was 10,000 shares of Altria at a price $34.35, so the investment has a value of $343,500. Also included were 7,295 shares of ABBV at an initial price of $48.45, 7,458 shares of EIX at $46.06, and 8161 shares of TXN at $42.09 (all equal positions, valued at $343,500 (all In US Dollars)).

The Approach with Altria

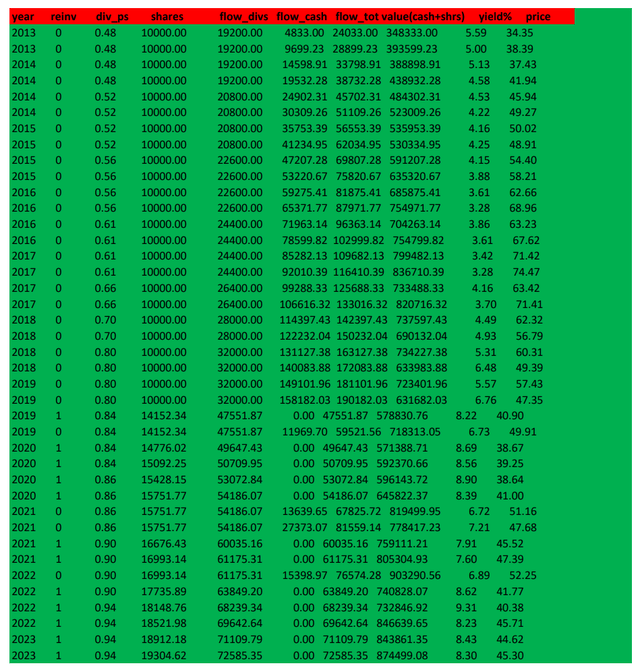

1. No Dividends Reinvested

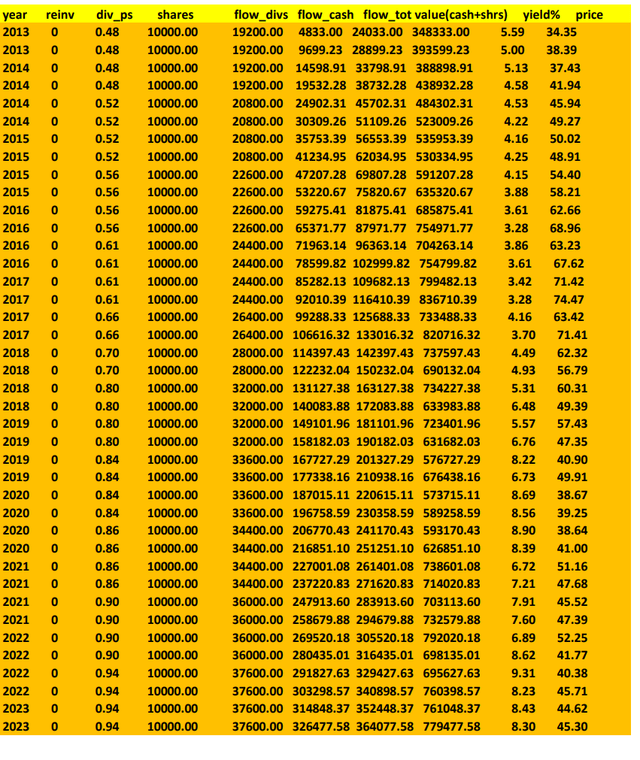

In this case, the shares are maintained steady and the dividends, when converted to cash are compounded at 2.75% and accumulated. Note that flow_divs are the yearly cash flow at that dividend level. flow_cash is the accumulated cash maintained in the portfolio associated with this stock and compounded yearly at 2.75%. I selected 2.75% as an average of Zero-Rate Interest Rate Policy and the current approximate fed funds rate of 5.5%. The stock value in US Dollars($) (cash + shares*price) is the total value within the portfolio associated with the single stock- current cash plus value of shares at current share price. flow_tot is the total “current cash flow” generated within the portfolio by accumulated cash and forward yearly cash dividends. Note also that there are other relevant columns for year, price, yield, and whether the dividends are reinvested or not (reinv indicator = 0, no reinvestment, revint =1 reinvest dividends)

Author’s Calculations, All Portfolio Values in USDollars($)

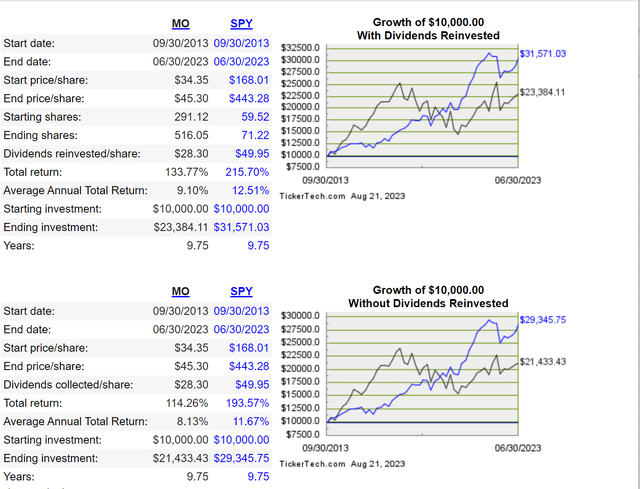

Now, to compare with an established model for an independent verification, I utilized an on-line dividend calculator which computes its own portfolio value for one stock starting out with the same investment. I have illustrated the result of this computation here. Here is a link to the website that presents the model for easy implementation.

Independent Dividend Calculator Model (dividendchannel.com)

Note that to compare correctly, I have taken the initial investment constrained by the independent model, which is $10,000, and scaled it up to the initial investment of the case being verified in question – which is a factor of 34.35 (and yields $343,500 as the initial investment). When this is done, the calculation results for the independent model case for no reinvestment of dividends when properly scaled up is 34.35 X $21,433.43 = $736,238.32. My model yielded $779,477.58, which differs by 5.87%. This discrepancy could have occurred due to the assumptions for what the cash is doing inside the portfolio. I assumed that it is reinvested at 2.75%. I do not know what the independent model is assuming. However, for more possible clarification and verification, I executed my model again with no dividend reinvestment but assuming that the cash is simply held without growth. When this is done, I derive the resulting chart shown below.

Author’s Calculations, All Portfolio Values in USDollars($)

Note that I computed here the portfolio stock value for the cash accumulating but not growing by an interest rate factor in the portfolio is $740,800. If I use the averages the two computed results in my model for no-reinvestment, the resulting value I obtain is ($740,800 + $779,477)/2 = $760,138.5, which now differs from the external independent model by $760,138.5/$736,238.32 = 3.246%. This still remains a bit high, and it may very well be that the independent model utilized close to Zero Interest Rate Policy yields. If this is the case, then a more accurate comparison would be closer to my case with no cash growth. The difference between these two cases is $740,800/$736,238.32 = 0.62%, which is more within an acceptable confidence range. Therefore, I conclude that this could serve reasonably as an independent check of my model validity for this case. Note that $740,800.00 as my final value would correspond to an annualized return of 8.201%, which is ($740,800/$343,500)^(1/9.75), where ^ is raise to power, 9.75-year investment interval. This is compared favorably with the independent model result of 8.13%.

2. All Dividends Reinvested

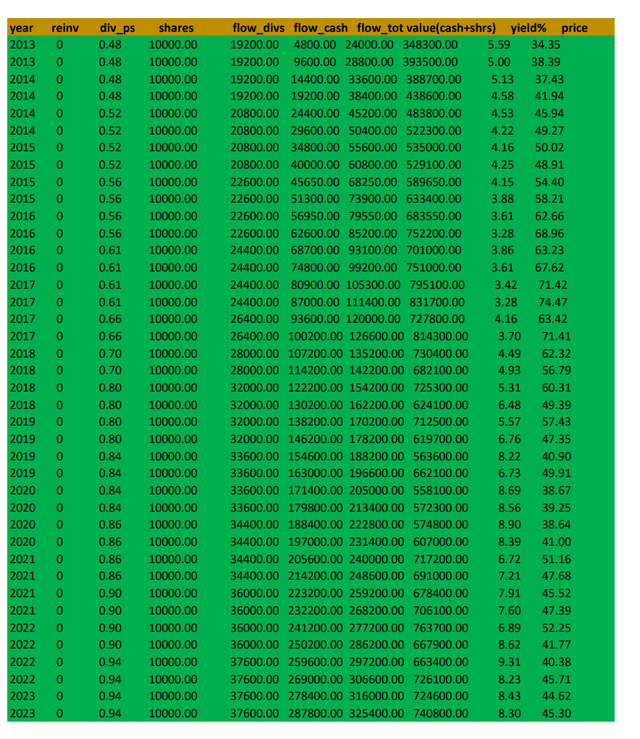

Next, moving onto the case with all MO dividends reinvested, my model produces the following result is chart form: (note that no cash associated with the stock is being accumulated because all dividends are reinvested as stock shares).

Author’s Calculations, All Portfolio Values in USDollars($)

Examining again the independent model for all dividends reinvested, shows that my computation yields $814,613.50 for a portfolio value, whereas the scaled independent model shown above yields $23,384.11 X 34.35 = $803,44.17 and therefore the two results differ by a factor of $814,613.50/$803,244.17 = 1.415%, and this discrepancy can be readily and reasonably caused by differing assumptions about the precise re-investment prices that were selected. Note that also, the annualized rate of return as computed by the independent model is 9.10%, to be favorably compared as shown below with the results of my model at 9.260%= ($814,613.50/$343,500)^(1/9.75)– ^ is raise to power, 9.75 year investment interval.

Based upon these independent verification checks for individual stocks that I have carried out with an established independent online model, the reader can be confident in my application of the current computational model for all cases going forward.

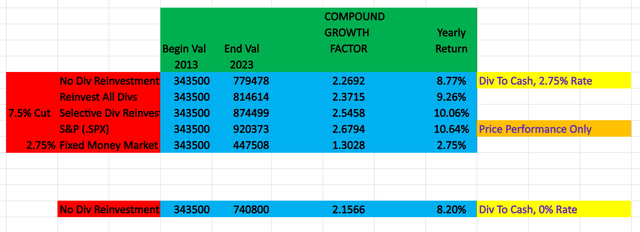

3. Hybrid Model with Reinvestment Yield Cut-Off at 7.5%

Finally, I executed my model for selected reinvestment for dividends, only when the stock yield is above 7.5%. This level can be adjusted according to investor preferences, and is not written in stone. I employed it here to best optimize the resulting portfolio value. The results are illustrated in the chart below.

Author’s Calculations, All Portfolio Values in USDollars($)

Note in this case a final portfolio value of $874,499.08. This represents a 7.4% improvement over the case where all dividends are reinvested = $874,499 /$814,613, and a 12.2% improvement over the case where no dividends are reinvested = $874,499.08/$779,477.58 (with 2.75% cash interest). The improvement in yearly annualized total return between no reinvestment to hybrid reinvestment is 10.06/8.77 = 14.71%. Note also that if the Zero Interest Rate Policy had been employed and was in effect for the no reinvestment case (all dividends to cash), the improvement in annualized return would have been 10.06/8.20= 22.6%. I have presented a table below summarizing all results:

Author’s Calculations, All Portfolio Values in USDollars($)

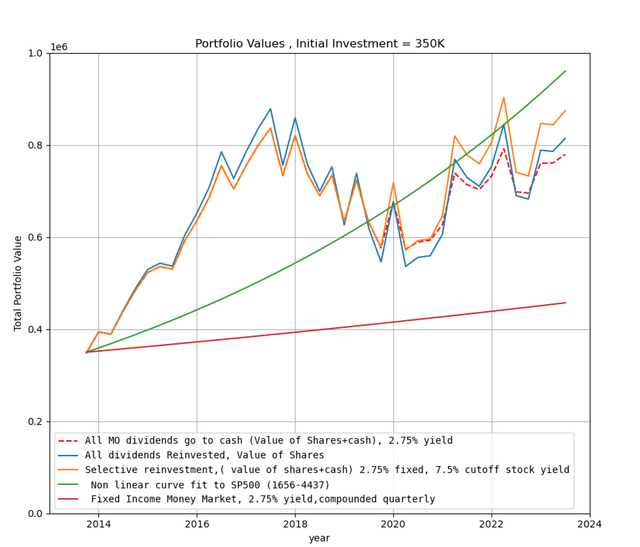

Lastly, I show a plot of all cases for further illustration to accompany the last chart for all the relevant cases. Note that the vertical scale is in millions of dollars.

Author’s Calculations, All Portfolio Values in USDollars($)

The Approach with AbbVie

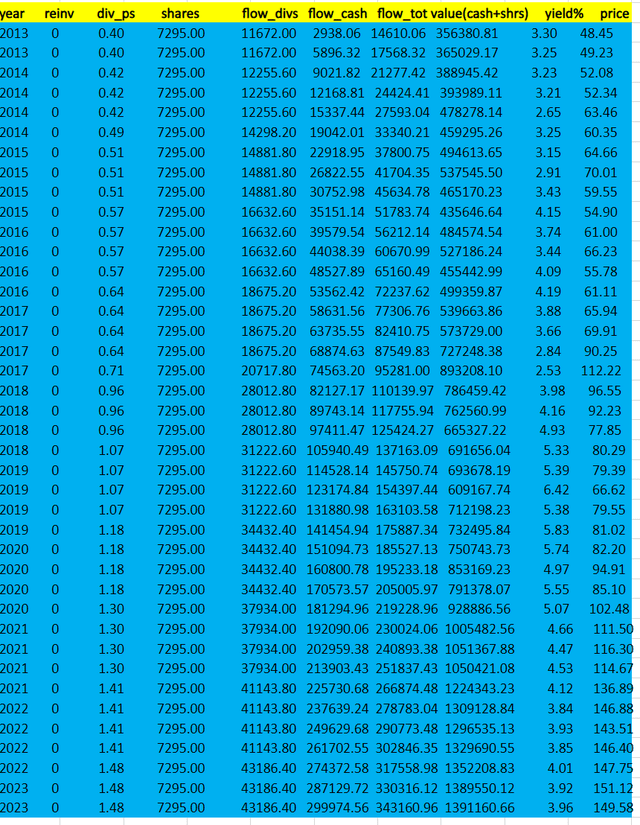

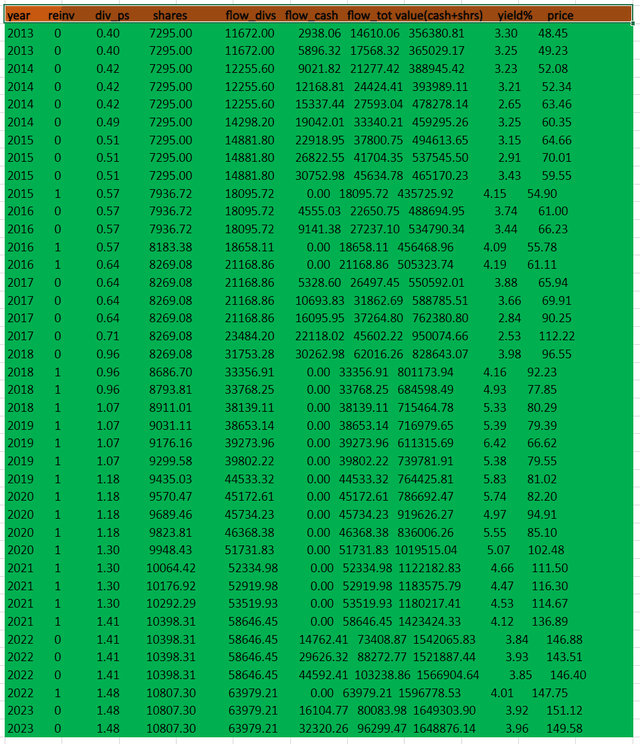

1. No Dividends Reinvested

I applied the same techniques to ABBV as I did to MO. In the case for no dividend reinvestment, here are the results for ABBV.

Author’s Calculations, All Portfolio Values in USDollars($)

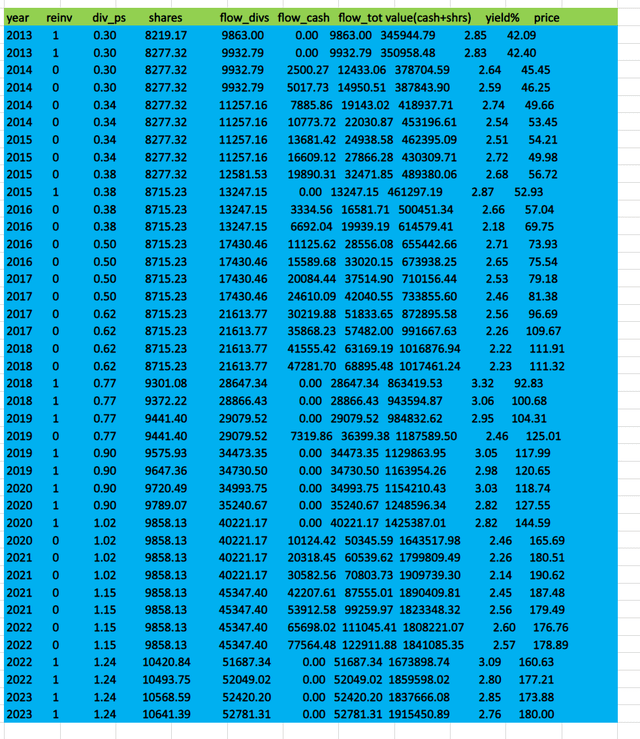

2. Hybrid Model

Here are my results for the hybrid model for ABBV. It turns out that for this stock, the hybrid method worked equally well for cut-offs ranging between 3% and 5%, so I have shown the 4% result here and have included the other hybrid comparative cases in graphical form. It turns out that for ABBV (as will be illustrated below), the reinvestment of dividends for most of the time interval worked quite well, and some of the hybrid cut-offs had results which overlapped each other.

Author’s Calculations, All Portfolio Values in USDollars($)

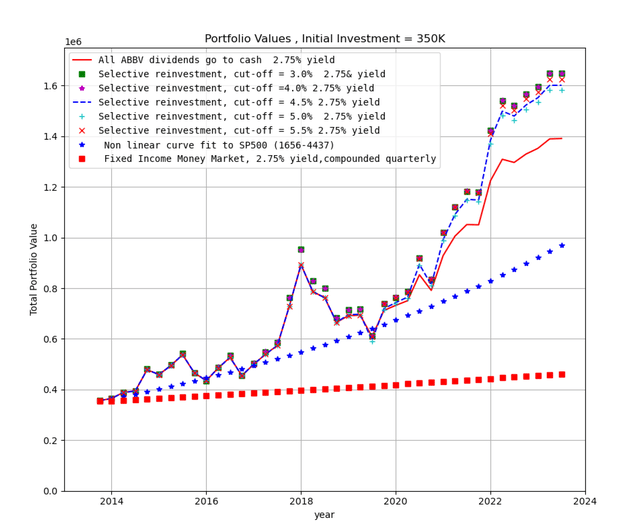

Here is a graphical summary that I generated, which includes all the hybrid cases for ABBV.

Author’s Calculations, All Portfolio Values in USDollars($)

In this particular case, the results were optimal for a cut-off of 3-4% as the results directly overlap. This is a consequence of the different numeric behavior for this particular stock. This is a stock which happened to perform quite well relative to the SP index, and had significantly better returns, which are summarized in the chart below.

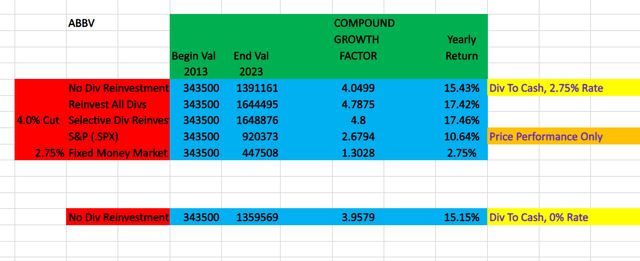

Author’s Calculations, All Portfolio Values in USDollars($)

Note in this case, for a 3-4% cut-off a final portfolio value of $1,648,876 and a total return of 17.46%. This represents only slight improvement over the case where all dividends are reinvested = $1,648,876 /$1,644,495= 1.00266, or 0.266%. This indicates that for ABBV, reinvestment of dividends (autopilot) can be considered as an alternatively preferred selection. Note that for the case (4% cut-off) there is an 18.525% improvement over the case where no dividends are reinvested = $1,648,876/$1,391,161 (with 2.75% cash interest). The improvement in yearly annualized total return between no reinvestment to hybrid reinvestment is 17.46/15.43 = 13.156%. Note that if I had employed a Zero Interest Rate Policy as the prevailing rate in effect for the no reinvestment case (all dividends to cash), the improvement in annualized return would have been 17.46/15.15= 15.248%.

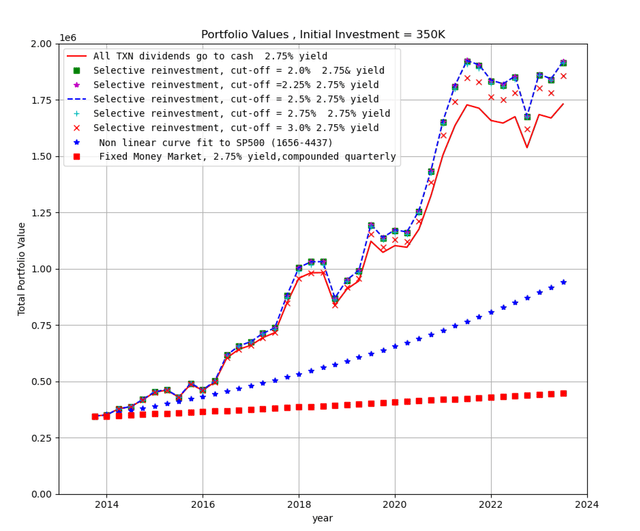

The Approach with Texas Instruments

1. Hybrid Model

Here are my results for the hybrid model for TXN. It turns out that for this stock, the hybrid method worked the best for a cut-off set at 2.75%, so I have shown the 2.75% result here and have included the other hybrid comparative cases in graphical form. It turns out that for TXN (as will be illustrated below), the reinvestment of dividends for most of the time interval worked quite well, for cut-off yields between 2 and 2.75% and some of the hybrid cut-offs had results which overlapped each other.

Author’s Calculations, All Portfolio Values in USDollars($)

Here is my graphical summary including all hybrid cases for TXN.

Author’s Calculations, All Portfolio Values in USDollars($)

In this particular case, the results were optimal for a cutoff of 2.5-2.75% as the results directly overlap. Again, this is a consequence of the different numeric behavior for this particular stock. This is another stock which happened to perform quite well relative to the SP index, and had significantly better returns, which are summarized in the chart below.

Author’s Calculations, All Portfolio Values in USDollars($)

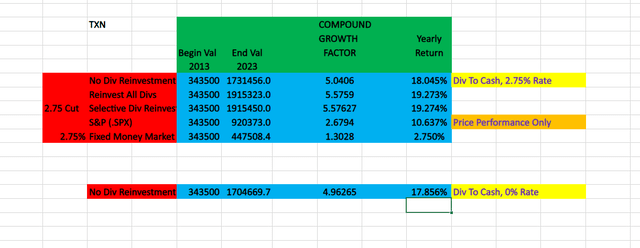

Note in this case, for a 2.75% cut-off a final portfolio value of $1,915,450 and a total return of 19.274%. This represents only very, very slight improvement over the case where all dividends are reinvested = $1,915,450 /$1,915,323= 1.00007, or 0.007%. This indicates that for TXN, reinvestment of dividends was the solidly preferred selection. Note that for the case (2.75% cut-off) there is a 10.626% improvement over the case where no dividends are reinvested = $1,915,450/$1,731,456.9 (with 2.75% cash interest). The improvement in yearly annualized total return between no reinvestment to hybrid reinvestment is 19.274/18.045 = 6.811%. Note that if I utilized a Zero Interest Rate Policy to have been in effect for the no reinvestment case (all dividends to cash), the improvement in annualized return would have been 19.274/17.856 = 7.941%.

The Approach With Edison International

1. Hybrid Model

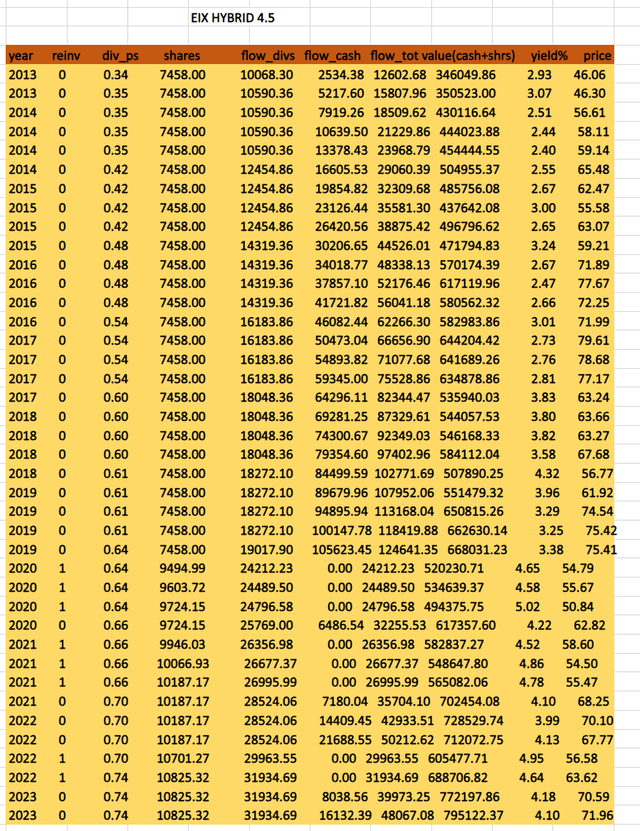

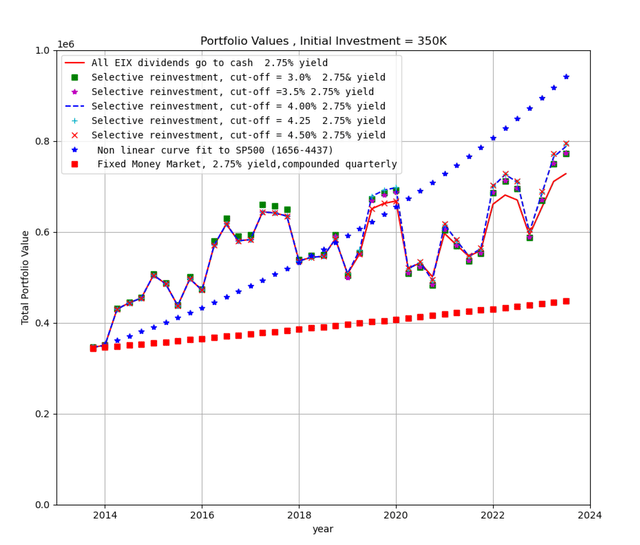

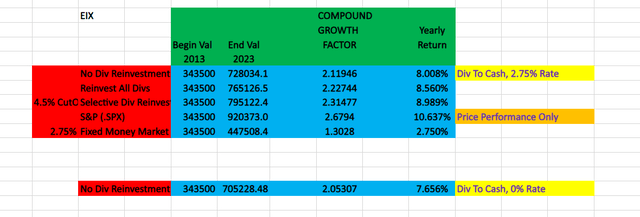

Here are my results for the hybrid model for EIX. It turns out that for this stock, the hybrid method worked the best for a cut-off set at 4.50%, so I have shown the 4.5% result here and have included the other hybrid comparative cases in graphical form. It turns out that for EIX (as I have illustrated below), the reinvestment of dividends for most of the time interval worked quite well, for cut-off yields between 3 and 4.5% and some of the hybrid cut-offs had results which overlapped each other.

Note that for EIX, the dividends were paid out in fractions of a penny, so in archiving and showing these tables for EIX, there are rounding truncations which alter the data slightly. For instance, .34 was actually .3375, so that explains the error that you may think occurs when you multiply .34 X 7458 X 4=10142.30, but it’s actually .3375 X 4 X 7458 = 10,068.30, correct as shown.

Author’s Calculations, All Portfolio Values in USDollars($)

Here is my graphical summary, including all hybrid cases for EIX.

Author’s Calculations, All Portfolio Values in USDollars($)

In this particular case, the results are seen to be optimal for a cutoff of 4.0-4.5% as the results directly overlap. Again, this is a consequence of the different numeric behavior for this particular stock. This is a stock which also underperformed relative to the SP index, by more than MO did, and had somewhat lower returns. This is to be somewhat expected, as the latter were in the technology sector and EIX, MO are energy and consumer staple stocks.

Here is my final chart of all relevant cases for EIX.

Author’s Calculations, All Portfolio Values in USDollars($)

Note in this case, for a 4.50% cut-off a final portfolio value of $795,122 and a total return of 8.989% are achieved. This represents a modest improvement over the case where all dividends are reinvested = $795,122.4/$765,126.5= 1.0392, or 3.92%. Note that for the case (4.0% cut-off) there is a 9.215 % improvement over the case where no dividends are reinvested = $795,122.4/$728,034.1 (with 2.75% cash interest). The improvement in yearly annualized total return between no reinvestment to hybrid reinvestment is 8.989/8.008 = 12.25%. Note that if I had employed a Zero Interest Rate Policy to be in effect for the no reinvestment case (all dividends to cash), the improvement in annualized return would have been 8.989/7.656 = 17.411%. The benefits of dividend reinvestment (total or hybrid optimized) are fairly evident in this case.

Total Portfolio Performance for Optimized Reinvestment: MO, ABBV, TXN, EIX

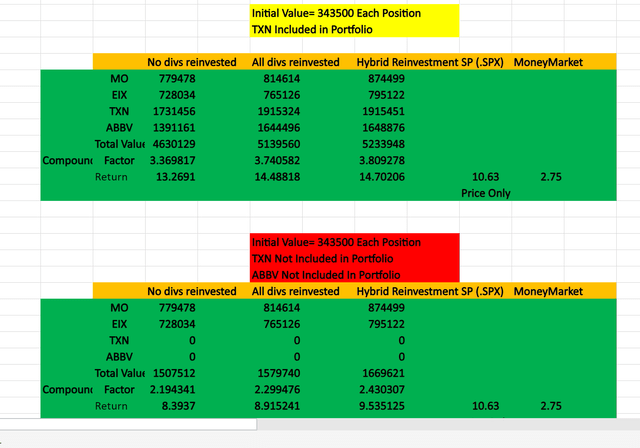

Lastly, I prepared a composite chart which illustrates the annualized total return of the entire portfolio for selected hybrid dividend reinvestment, (assuming that all positions were divided equally amongst all four stocks in the portfolio), as compared with the case in which all dividends are reinvested, and no dividends reinvested. I maintained the initial position of each stock maintained at $343,500. Upon examining the chart carefully, several conclusions can be arrived at concerning the value/utility of the hybrid reinvestment technique in a composite stock portfolio, versus just simply allowing all dividends to reinvest (autopilot) versus allowing all dividends to go to cash and be maintained in the portfolio along with stock shares. Here is the composite chart:

Author’s Calculations, All Portfolio Values in USDollars($)

In the top portion of this chart, I display the results at the end of the ten-year investing period. Note that the resulting annualized return for hybrid reinvestment is not significantly improved over the case of all dividends reinvested. The difference is 1.4%.(14.7006/14.48818). The reason for the closeness is the superior performance of TXN and ABBV during this time period – the yields remained fairly steady as the dividends were increased, so there were little differences between hybrid reinvesting and total reinvesting. Also, the returns of ABBV and TXN far exceeded that of MO and EIX and dominated the portfolio performance. MO and EIX had more significant swings in yield versus price, so the hybrid technique worked better for those stocks, individually. This is why I have included a bottom section which shows the performance with only MO and EIX, and in this case we get 7% improvement over the case of autopilot (9.53/8.91). Of course, this portfolio analysis does not include any impact of diverting cash from one position to another, either as the dividend, or the results of rebalancing the portfolios, which likely needs to be further addressed down the line. Simply holding cash and not reinvesting in any other position when opportunities are created may not be always a good strategy to invoke consistently.

A very important observation that one can make as a result of this study is that each stock in a portfolio needs to be thoroughly analyzed and characterized individually, employing the “hybrid technique”, to determine the initial optimal method of management for each stock as a component of that portfolio (as applied to selection of a cut-off for reinvestment). The hybrid cut-off needs to be very carefully optimized for each stock, and I arrived at this level by approximation and I did not rigorously carry out any separate optimization here. As mentioned above, further additional improvements in the portfolio performance may be carried out by consideration of diverting cash from one investment held with the stock value to another position. This can possibly be the subject of future articles and investigations as more/alternative stocks with similar characteristics to MO, ABBV, TXN, and EIX will be selected from entirely different sectors.

Risks and Limitations

As I have begun to explore and discuss above, there are some limitations to the implementation of this strategy in a successful and enduring portfolio design. For instance, the hybrid yield level I selected for each stock in this study was chosen by my inspection and approximation of the yield distribution and behavior for the investment period I considered for each stock. Often, there are either patterns where the yield distribution is steady or oscillates considerably and each of these cases needs to be further addressed for optimal selection of a cut-off level. Furthermore, there can be very large differences in the performances of selected stocks included in the final portfolio. This phenomenon can swing and stilt the performance in the direction of the superior performing stocks, in spite of the less valued and weighted performance of the other sticks, which can mask the effects of the optimal selection of cut-off yields of these underperforming stocks. Finally, the study that I carried out makes no specific assumption as to the due diligence that needs to be carried out preliminarily for selecting solid underlying businesses whose balance sheets and free cash flow profiles are worthy of consideration as candidates for carrying out this analysis. I did conduct reasonable assessments for stock selection based upon standard guidelines and other analysts; opinions already available, and my detailed investment experiences over 25 plus years. Since my background is less financial accounting/business/balance sheet oriented, and more in the category of numerical analysis, engineering and mathematics, the study largely incorporates and concentrates upon a consideration primarily of numerical and statistical patterns in chart data.

Conclusion and Final Thoughts

I have presented an analysis for optimizing individual stock performance utilizing a hybrid cut-off yield portfolio optimization technique which selectively reinvests cash and dividends of individual portfolio stocks in accordance with favorably-derived stock yield cut-off levels. I have demonstrated that for individual companies under consideration, the technique will greatly improve the stock performance by as must as 15% over a case where either no dividends are reinvested or an “autopilot”, wherein all dividends in a stock are continuously reinvested, regardless of stock yield. When all stocks are optimized in this fashion and included in a composite portfolio, there is a major improvement over the case where no dividends are reinvested and held as cash, but a less beneficial effect is observed over the autopilot case, especially if some of the stocks dominate the performance, or exhibit more steady patterns in their stock yield distribution (less oscillations, individual distinct cycles and swings over the investment period under consideration).

I am is currently maintaining a significant long position in Altria, AbbVie, Texas Instruments, and Edison International within a retirement account and another smaller position in a brokerage account outside of retirement.

{kind=link}